Featured

Table of Contents

- – What is the most popular Annuity Payout Option...

- – What is the difference between an Immediate An...

- – How do I get started with an Annuities For Re...

- – What does a basic Tax-deferred Annuities plan...

- – How do I apply for an Guaranteed Return Annu...

- – How do Tax-efficient Annuities provide guara...

Keep in mind, nevertheless, that this does not say anything concerning readjusting for inflation. On the bonus side, also if you assume your option would certainly be to buy the supply market for those seven years, which you 'd obtain a 10 percent yearly return (which is far from certain, specifically in the coming decade), this $8208 a year would be greater than 4 percent of the resulting nominal stock value.

Example of a single-premium deferred annuity (with a 25-year deferral), with four payment alternatives. The regular monthly payout below is highest possible for the "joint-life-only" alternative, at $1258 (164 percent higher than with the instant annuity).

The way you purchase the annuity will certainly figure out the answer to that inquiry. If you purchase an annuity with pre-tax bucks, your premium decreases your taxable income for that year. According to , buying an annuity inside a Roth strategy results in tax-free repayments.

What is the most popular Annuity Payout Options plan in 2024?

The advisor's very first step was to develop a thorough monetary prepare for you, and after that discuss (a) just how the suggested annuity matches your total strategy, (b) what choices s/he thought about, and (c) just how such alternatives would certainly or would certainly not have actually led to reduced or higher settlement for the consultant, and (d) why the annuity is the exceptional choice for you. - Secure annuities

Obviously, an advisor may attempt pressing annuities even if they're not the finest fit for your circumstance and goals. The reason could be as benign as it is the only product they market, so they drop victim to the typical, "If all you have in your toolbox is a hammer, pretty soon everything begins resembling a nail." While the consultant in this scenario may not be unethical, it boosts the threat that an annuity is an inadequate option for you.

What is the difference between an Immediate Annuities and other retirement accounts?

Since annuities frequently pay the agent marketing them much greater payments than what s/he would get for investing your cash in mutual funds - Annuity withdrawal options, allow alone the absolutely no compensations s/he 'd get if you purchase no-load common funds, there is a big motivation for agents to press annuities, and the extra complicated the much better ()

An underhanded expert recommends rolling that quantity into brand-new "better" funds that just take place to lug a 4 percent sales tons. Accept this, and the expert pockets $20,000 of your $500,000, and the funds aren't most likely to carry out much better (unless you chose even much more badly to start with). In the very same instance, the expert could guide you to acquire a complex annuity with that $500,000, one that pays him or her an 8 percent payment.

The expert hasn't figured out how annuity repayments will certainly be taxed. The expert hasn't disclosed his/her settlement and/or the costs you'll be billed and/or hasn't shown you the impact of those on your ultimate repayments, and/or the compensation and/or costs are unacceptably high.

Your family background and existing health factor to a lower-than-average life expectancy (Annuity interest rates). Existing rate of interest, and hence projected settlements, are traditionally reduced. Even if an annuity is right for you, do your due diligence in comparing annuities sold by brokers vs. no-load ones sold by the providing business. The latter may need you to do even more of your very own research study, or utilize a fee-based financial advisor that may get compensation for sending you to the annuity provider, but might not be paid a higher compensation than for various other investment alternatives.

How do I get started with an Annuities For Retirement Planning?

The stream of monthly payments from Social Protection resembles those of a postponed annuity. A 2017 comparative evaluation made a thorough comparison. The following are a few of the most significant factors. Considering that annuities are voluntary, the individuals acquiring them typically self-select as having a longer-than-average life span.

Social Protection benefits are fully indexed to the CPI, while annuities either have no inflation security or at most supply an established percentage yearly increase that may or may not compensate for rising cost of living completely. This type of rider, just like anything else that raises the insurance firm's risk, requires you to pay even more for the annuity, or accept reduced settlements.

What does a basic Tax-deferred Annuities plan include?

Please note: This write-up is intended for informational objectives only, and must not be thought about monetary recommendations. You must speak with a monetary expert before making any significant economic choices. My career has actually had many unforeseeable spins and turns. A MSc in academic physics, PhD in experimental high-energy physics, postdoc in fragment detector R&D, research placement in experimental cosmic-ray physics (including a number of sees to Antarctica), a short job at a little engineering solutions business supporting NASA, complied with by beginning my very own small consulting technique supporting NASA projects and programs.

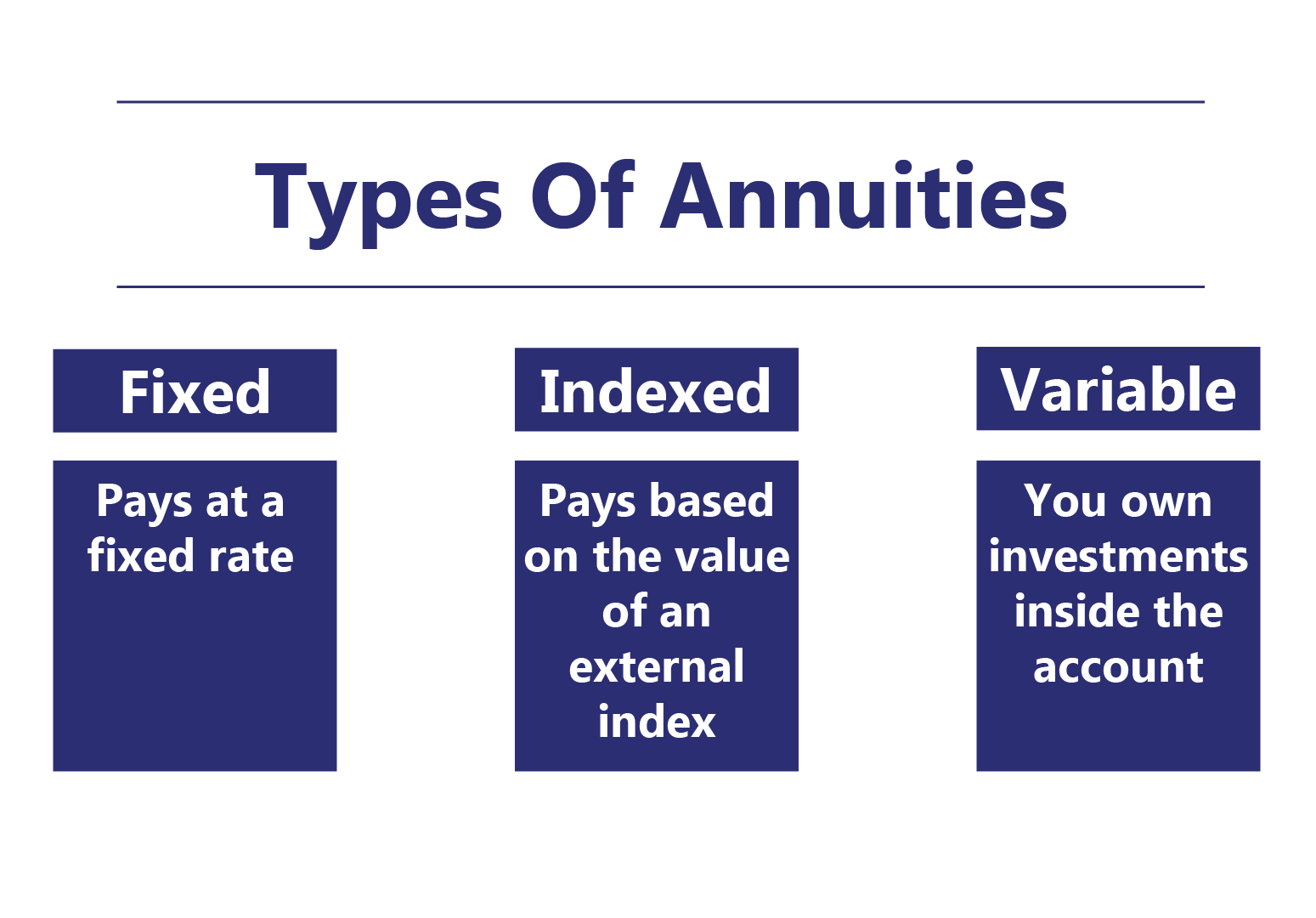

Given that annuities are intended for retired life, taxes and penalties might apply. Principal Defense of Fixed Annuities. Never ever shed principal due to market performance as taken care of annuities are not purchased the market. Also during market downturns, your money will not be affected and you will certainly not lose cash. Diverse Financial Investment Options.

Immediate annuities. Utilized by those that desire reputable income promptly (or within one year of acquisition). With it, you can tailor earnings to fit your needs and produce earnings that lasts forever. Deferred annuities: For those who desire to expand their money gradually, however agree to delay accessibility to the cash up until retirement years.

How do I apply for an Guaranteed Return Annuities?

Variable annuities: Supplies better potential for growth by investing your cash in financial investment options you pick and the capacity to rebalance your profile based on your choices and in such a way that aligns with altering economic goals. With taken care of annuities, the firm invests the funds and supplies a rates of interest to the client.

When a death claim happens with an annuity, it is essential to have actually a called recipient in the contract. Various alternatives exist for annuity survivor benefit, depending on the contract and insurance provider. Choosing a reimbursement or "period certain" choice in your annuity gives a survivor benefit if you die early.

How do Tax-efficient Annuities provide guaranteed income?

Calling a beneficiary various other than the estate can assist this process go extra efficiently, and can help make certain that the proceeds go to whoever the specific desired the cash to go to rather than going via probate. When existing, a fatality advantage is automatically consisted of with your agreement.

{kind=link}

Table of Contents

- – What is the most popular Annuity Payout Option...

- – What is the difference between an Immediate An...

- – How do I get started with an Annuities For Re...

- – What does a basic Tax-deferred Annuities plan...

- – How do I apply for an Guaranteed Return Annu...

- – How do Tax-efficient Annuities provide guara...

Latest Posts

Highlighting Fixed Vs Variable Annuity Pros Cons A Closer Look at Fixed Index Annuity Vs Variable Annuities What Is Fixed Index Annuity Vs Variable Annuity? Features of Smart Investment Choices Why Ch

Analyzing Variable Annuities Vs Fixed Annuities Everything You Need to Know About Financial Strategies Breaking Down the Basics of Fixed Vs Variable Annuities Advantages and Disadvantages of Different

Analyzing Deferred Annuity Vs Variable Annuity Key Insights on Choosing Between Fixed Annuity And Variable Annuity Defining the Right Financial Strategy Features of Smart Investment Choices Why Choosi

More

Latest Posts